Lately I’ve been having a lot of conversations around investment terms with searchers, as well as investors.

About 15 years ago, I interned at a search fund. And, over the last few years, I’ve started to invest in the asset class going direct as well as through funds of search funds.

Investing in search funds is a great way to scratch my entrepreneurial itch, extremely rewarding when a searcher finds success, and can be economically rewarding too.

This post is my attempt to share thoughts on self funded search economics in an effort to contribute to the search fund community, get feedback on my thinking from a wider audience, and of course meet more people who are doing searches/investing and may want to collaborate (please feel free to reach out!).

You can watch a video of me explaining this model here, and download the excel here:

Enterprise Value

The standard finance equation is enterprise value = debt + stock – cash. Enterprise value is how much the company itself is worth. Many times people confuse it with how much the stock is worth and find the “minus cash” part of this really confusing.

So, you can rearrange this equation to make it stock = enterprise value – debt + cash. Make more sense now?

Enterprise value is just how much you’re willing to pay for the company (future cash flows, intellectual property, etc), not the balance sheet (debt and cash).

Most investors and searchers think about the EBITDA multiple of a company on an enterprise value basis because they’ll be buying it on a cash free, debt free basis. It becomes second nature to think about EBITDA multiples and know where a given business should fall given scale, industry, etc.

However, I believe this second nature way of thinking of things can be a massive disadvantage to investors given the way EV and multiples are talked about in our community currently.

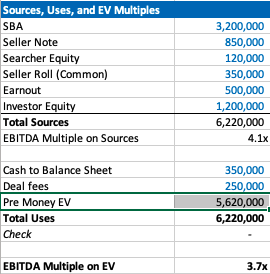

Sources of capital, the typical way to calculate enterprise value for self funded searchers

If you’ve ever looked at or put together a teaser for a self funded search deal, you will notice that the deal value is equal to the sum of the sources of capital minus deal fees and cash to the balance sheet.

As a simple example, if there is $4 mm of debt to fund the deal, $1 mm of equity, and $200k of deal fees, the enterprise value = $4 mm + $1 mm – 200k = $4.8 mm.

We’ll use slightly more complex numbers in our example: If a searcher is taking a $3.2 mm SBA loan, $850k seller note, putting in $120k themselves, getting $350k of equity from the seller, a $500k earnout, and $1.2 mm of equity financing minus $350k to the balance sheet and $250k of deal fees, then the enterprise value will be $5.62 mm.

Our example company has $1.5 mm of EBITDA, so the EBITDA multiple is 3.7x. This is a pretty attractive acquisition multiple for a business that meets traditional search criteria (recurring revenues, fragmented competition, high gross margins, low customer concentration, etc).

If you’re seeing a search fund deal for the first time, the headline of “we’re buying a decent company for 3.7x, and replacing a tired owner with a hungry operator” is pretty exciting!

However, if you’re an investor, there is some nuance to this enterprise value number and the true EBITDA multiple you are investing in.

The trick with self funded enterprise value

The security that most self funded search investors get in a deal is participating preferred stock with a paid in kind dividend. This means when there’s an exit, you get your money back before any other equity holder, then get a certain percent of the business, and whatever dividend you’ve been owed in the interim accrues to your principle.

It’s a really favorable security for the investor, and one that is basically impossible to get in VC where straight preferred stock is much more common (no pun intended).

The key terms are what percent of common equity does this security convert into after the originally principal is paid back, and what is the dividend.

The share of common equity the investor group will get typically ranges from 10-50% of the total common stock. The dividend rate is usually 3-15%. The average I’m seeing now is around 30% and 10% for common and dividends respectively.

The strange this about the enterprise value quoted to investors in a teaser/CIM is that it doesn’t change as the percent of common changes, even though this has large implications for how much the common equity is worth and the value investors receive.

For example, I may get a teaser where the sources of investment – cash to balance sheet – deal fees = $3.7 mm for a $1 mm EBITDA company, which would imply a 3.7X EBITDA multiple. Let’s say the searcher is offering investors 30% of the common and a 10% dividend.

Let’s now say that the searcher is having a tough time raising capital and changes their terms to 35% of common and a 12% dividend. Does the effective enterprise value change for investors? I would argue yes, but I would be surprised to see it changed in the CIM/teaser.

This isn’t a knock on searchers or the search fund community. It’s just kind of how things are done, and I think this is mostly because it’s really hard to think about how the enterprise value has changed in this scenario.

However, the natural way of using EBITDA multiples to think about value for a business that is so common in PE/SMB can be extremely misleading for investors here. You may be thinking 3.7X for this type of business is a great deal! But, what if the security you’re buying gets 5% of the common?

If you’re in our world, you may counter this point by saying most searchers will also supply a projected IRR for investors in their CIM. However, IRR is extremely sensitive to growth rate, margin expansion, and terminal value. While the attractiveness of the security will be reflected, it can be greatly overshadowed by lofty expectations.

To get more clarity and have a slightly different mental model on the effective price investors are paying for this business, let’s go back to basics. Enterprise value should be debt + preferred stock + common stock – cash.

We know the values of each of these numbers, except the common. So, the main question here becomes: how much is the common equity worth?

Calculating value of common equity for self funded search funds

Equity value for most search fund deals = preferred equity from investors + the common equity set aside for the searcher and sometimes also advisors, board, seller.

We know that the preferred equity is investing a certain amount for a certain amount of common equity. The rub is that they are also getting a preference that they can take out before any common equity gets proceeds, and they are getting a dividend.

So, the exercise of valuing the common equity comes down to valuing the preference and dividend.

In my mind, there are three approaches:

- The discount rate method where you take the cash flows you’ll get in the future from the pref/dividends and discount them back at the discount rate of your choice. I am using 30% in my model which I believe accurately compensates investors for the risks they are taking in a small, highly leveraged investment run by an unproven operator. If you believe in efficient markets, this number also fits as it mirrors the historical equity returns as reported by the Stanford report, with a slight discount given this asset class has clearly generated excess returns relative to other assets on a risk adjusted basis, hence interest in these opportunities from an expanding universe of investors.

- The second method is to calculate how much money you’d get from your preference and dividends, taking into account that per the Stanford study around 75% of search funds will be able to pay these sums, and then discount these cash flows back at a rate more in line with public equities (7% in my model). This yields a much higher value to the preference/dividend combo, and therefore lowers the implied value of the common equity.

- The last method is to just say nope, there is no value to the preference and dividend. I need them and require them as an investor, but they are a deal breaker for me if they aren’t there, and therefore they don’t exist in my math. This of course makes no logical sense (you need them, but they also have no value?), but I’ve left it in as I think many investors probably actually think this way and it creates a nice upper bound on the enterprise value. Side note, as with obstinate sellers, jerk investors are usually best avoided.

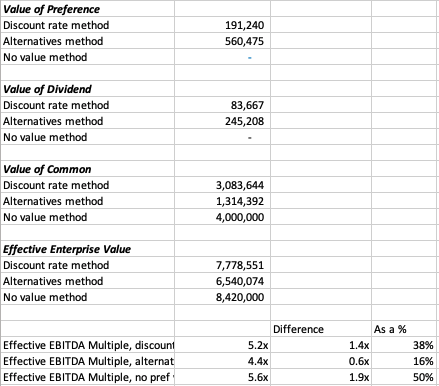

In our example, you can see a breakdown of the preference value, dividend value, and therefore common value and enterprise value for this deal.

In each case, the effective EBITDA multiple moves from 3.7x to something much higher (see the last 3 lines).

There are some simplifying assumptions in the model (no accruing dividend, all paid in last year), and some weird stuff that can happen (if you make the hold time long and the dividend greater than the 7% equity discount rate, the value of the dividend can get really big).

These flaws aside, I think this creates a nice framework to think through what the common is actually worth at close, and therefore what enterprise value investors will be paying in actuality.

It’s worth noting that the whole point of this is to benchmark the value you’re getting relative to market transactions in order to understand where you want to deploy your capital.

This creates a method to translate cash flow or EBITDA multiples of other opportunities on an apples to apples basis (if only there were a magical way to translate the risk associated with each as well!).

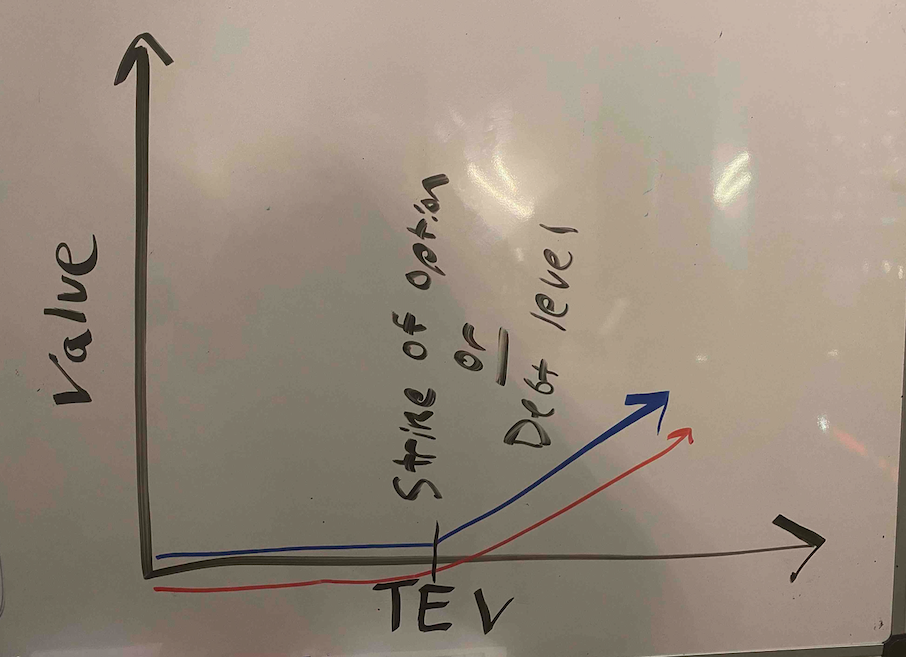

Another note, we could calculate the value of the common to be what this asset would trade at market today in a well run auction process minus any obligations (debt, preference, seller financing). However, I think that understates the option value inherent in this equity, a value that is only realized when a new manager takes over with more energy and know how.

There is a finance nerd rational for this. If you plot the value of equity in a leveraged company on a chart, it mirrors the payout of a call option. In both cases, the value of the security increases at a certain inflection point: when the value of equity rises above the strike price in an option, and when the enterprise value of a company rises above the debt level in a levered company.

The common equity of a highly levered company can therefore be valued by a similar methodology as the call option: Black Scholes. If you remember back to finance class, increasing volatility will increase the value of an option.

In the search fund case, we’ve (hopefully) increased the (upside) volatility and therefore create more value than simply selling the company today.

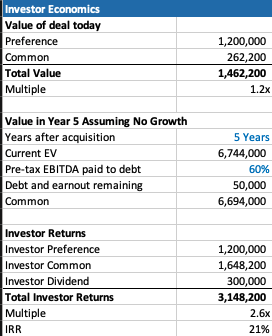

A few more thoughts on investor economics

There are a few other ways to think about the economics you get as an investor to best understand if this is the deal for you.

First, you may want to think about how much your investment will be worth day 1. The key lever in this model is what discount this company is being bought for relative to fair market value. For example, the searcher may have proprietary sourced a great company and is buying it for 25% below what it would trade at in a brokered auction.

This is very much a “margin of safety” philosophy on things. Same with the calculation on how much you’ll receive in year 5 (after QSBS hits) assuming no growth in the business.

The only problem with each of these calculations is that they never play out in practice. Most companies don’t just stay the same, you’re either in a rising tide or you’re in trouble. And, you’re almost never going to sell in year 1, and definitely not for a slight premium to what it was bought for.

However, if your investment is worth 30% higher day one, and you can make a 20% IRR assuming nothing too crazy happens either way in the business, that’s not a bad place to start. Add in a strong searcher, decent market, some luck, and you’re off to the races.

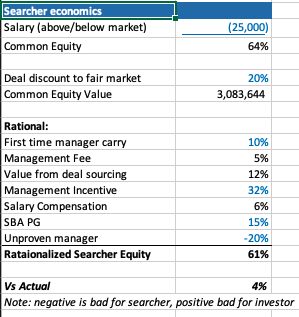

Thoughts on searcher economics

A lot of this post has considered things from the investor perspective as my main quandary was related to how to create an EBITDA multiple that made sense for investors.

However, the point of this post is not to say searchers are misrepresenting or being unrealistic with their terms. In fact, I think it’s quite logical that self funded searchers capture the massive economic value that they do.

There are many reasons why self funded searchers deserve the lion share of the common equity.

First, they are providing a nice service of giving investors a positive expected value home to park their money with much lower correlation to the market than other asset classes ($1 mm EBITDA companies don’t see lots of multiple contraction/expansion throughout cycles).

Most money managers that fit that criteria are taking a 2/20, of course they also usually have a track record. So, I’ve used a 10% carry in my model, but stuck to 2% annual management fee.

The searcher spent a lot of time, and probably money, finding this company. That’s a lot of value, especially if it’s a below market price. They should be able to capture a lot of the value in finding a below market deal.

The searcher may be taking a below market salary, and needs to get comped like any CEO, with stock options. In my example model I have $1 mm of stock vesting over the hold period, as well as extra comp for taking a below market salary.

Searchers are also usually putting their financial standing at risk by taking a personal guarantee on the bank/SBA loan. This is really tough to put a number on, as is the last line in my framework where searchers are dinged for lack of experience. Like any good model, you need a few lines that you can fudge to make the math work 🙂

What you do think?

I’m shocked that I wrote all this. I was going to type a few paragraphs and a quick excel. However, putting this to paper has been a great exercise for me to sharpen my thinking.

Now I’d like you to help me further. Where do you think this should be changed in this framework? How do you think about things from the investor and/or searcher side?

Feel free to shoot me a note if you have thoughts (even just to tell me I’m being way too academic with this, which I actually agree with).

Lastly, a post like this is really a trap I’m putting on the internet to catch any like minded people in so that we can figure out ways to collaborate now or in the future. So, at the very least, connect with me on LinkedIn 🙂

Greetings! I know this is kinda off topic but I’d figured I’d ask.

Would you be interested in exchanging links or

maybe guest writing a blog post or vice-versa? My website goes over a lot of the

same subjects as yours and I think we could greatly benefit

from each other. If you are interested feel free to

shoot me an e-mail. I look forward to hearing from you!

Superb blog by the way!

Hey there! I just wanted to ask if you ever

have any trouble with hackers? My last blog (wordpress) was hacked and I ended

up losing a few months of hard work due to no data backup.

Do you have any methods to prevent hackers?

Awesome issues here. I am very happy to see your article.

Thank you so much and I’m looking forward to touch you.

Will you please drop me a e-mail?

Greetings! This is my first comment here so I just wanted to give a quick shout out and tell you

I truly enjoy reading your posts. Can you suggest any other blogs/websites/forums that deal

with the same subjects? Thanks for your time!

We are a group of volunteers and opening a new scheme in our community.

Your website provided us with valuable information to work on. You’ve done a formidable job and our entire community will be grateful to you.

What’s up, I desire to subscribe for this webpage to

obtain most recent updates, thus where can i

do it please help.

Excellent blog here! Additionally your site lots up fast!

What web host are you using? Can I get your affiliate hyperlink in your host?

I wish my site loaded up as fast as yours lol

Thankfulness to my father who told me about this web site, this web site is

actually amazing.

I have read some excellent stuff here. Certainly worth bookmarking for revisiting.

I surprise how so much effort you set to create

any such fantastic informative web site.

Good way of describing, and good paragraph to get information regarding my presentation focus, which i am going

to convey in school.

Greetings! I’ve been reading your site for some time now and finally got the bravery to go ahead and give you a shout out from Austin Texas!

Just wanted to tell you keep up the fantastic job!

What’s up Dear, are you genuinely visiting this website regularly, if so afterward you

will without doubt get good experience.

Hey there! I know this is somewhat off-topic but I had to ask.

Does running a well-established blog such as yours require a lot of

work? I am brand new to blogging but I do write in my diary every day.

I’d like to start a blog so I can easily share my

experience and feelings online. Please let me know if you have any kind of recommendations or tips

for brand new aspiring blog owners. Thankyou!

Oh my goodness! Incredible article dude! Thank you so much, However I am having problems with your RSS.

I don’t understand why I can’t subscribe to it. Is there anyone else having the same RSS

problems? Anybody who knows the solution can you kindly respond?

Thanx!!

Awesome post.

whoah this blog is magnificent i like studying your posts. Stay

up the good work! You know, lots of people are searching

round for this info, you can help them greatly.

Why users still make use of to read news papers when in this technological world everything is available on web?

hi!,I like your writing so much! percentage we be in contact

more about your article on AOL? I require an expert in this space to resolve my problem.

Maybe that’s you! Looking forward to peer you.

I think the admin of this website is actually working hard in favor of his web site,

for the reason that here every material is

quality based material.

Excellent post. I was checking continuously this

blog and I am impressed! Very helpful information specially the last

part 🙂 I care for such information a lot. I was looking for this particular info for a very long time.

Thank you and good luck.

I constantly emailed this blog post page to all my associates,

for the reason that if like to read it after that my contacts will too.

Excellent post. I used to be checking constantly this weblog and

I am impressed! Extremely useful info specially the last section 🙂 I care for such info a lot.

I was looking for this certain information for a very long time.

Thanks and best of luck.

Does your website have a contact page? I’m having a tough time locating it

but, I’d like to shoot you an e-mail. I’ve got

some suggestions for your blog you might be interested in hearing.

Either way, great website and I look forward to seeing it develop over time.

What a stuff of un-ambiguity and preserveness of precious experience

on the topic of unpredicted emotions.

Truly when someone doesn’t understand afterward its up to other viewers

that they will help, so here it occurs.

Hey I know this is off topic but I was wondering

if you knew of any widgets I could add to my blog that automatically tweet my newest twitter updates.

I’ve been looking for a plug-in like this for quite some time and

was hoping maybe you would have some experience with something like this.

Please let me know if you run into anything. I truly enjoy reading your blog and I look forward to your new updates.

I know this if off topic but I’m looking into starting my own blog and

was wondering what all is needed to get set up?

I’m assuming having a blog like yours would cost a pretty penny?

I’m not very web smart so I’m not 100% positive. Any recommendations or advice would be greatly appreciated.

Appreciate it

It’s very effortless to find out any matter on web

as compared to books, as I found this paragraph

at this website.

Hi, i think that i saw you visited my blog thus i came to “return the

favorâ€.I am trying to find things

to improve my web site!I suppose its ok to use some of your ideas!!

What’s up, every time i used to check weblog posts here

in the early hours in the daylight, for the reason that

i love to learn more and more.

Great items from you, man. I’ve take into account your stuff prior to and you’re simply too excellent.

I actually like what you’ve got right here, certainly like

what you are stating and the way in which during which you are

saying it. You are making it entertaining and you continue to take care of to stay it wise.

I cant wait to learn far more from you. That is really a great web site.

Fastidious answers in return of this issue with

genuine arguments and explaining all about that.

I think that everything posted was very logical. However, consider this, what if you added a

little content? I am not suggesting your information isn’t good., but suppose you added

a post title that grabbed people’s attention? I mean Thoughts

on Search Fund Economics – Phil Strazzulla's Blog is a

little vanilla. You should glance at Yahoo’s front page and note how they

create article headlines to grab viewers to click.

You might add a related video or a pic or two to

get people excited about everything’ve got to say.

In my opinion, it could bring your website a little livelier.

Howdy! This post couldn’t be written any better!

Reading through this post reminds me of my good old room mate!

He always kept chatting about this. I will forward this article to him.

Fairly certain he will have a good read. Many thanks for sharing!

whoah this weblog is wonderful i really like reading your posts.

Stay up the good work! You know, lots of persons are searching around for this info,

you could aid them greatly.

Hi there! I just would like to offer you a big thumbs up

for the excellent info you’ve got here on this post. I will be returning to your

site for more soon.

Please let me know if you’re looking for a writer for your site.

You have some really good posts and I believe I would be a good asset.

If you ever want to take some of the load off, I’d really like to write

some articles for your blog in exchange for a link back

to mine. Please blast me an e-mail if interested. Regards!

certainly like your web site however you need to take a look at the spelling

on quite a few of your posts. A number of them are

rife with spelling issues and I to find it very troublesome to tell the truth however I will surely come back again.

Howdy! I know this is kinda off topic nevertheless I’d figured I’d ask.

Would you be interested in trading links or maybe

guest authoring a blog post or vice-versa? My site goes over a lot of the same subjects as yours and I feel we could

greatly benefit from each other. If you happen to be interested

feel free to send me an email. I look forward to hearing from you!

Awesome blog by the way!

Your means of explaining all in this piece of writing is in fact pleasant, every one

can effortlessly be aware of it, Thanks a lot.

You need to take part in a contest for one of the finest blogs on the web.

I am going to highly recommend this site!

Appreciate this post. Will try it out.

I am really impressed with your writing skills as well as with the layout on your blog.

Is this a paid theme or did you customize it yourself?

Anyway keep up the excellent quality writing, it is rare to see a great blog like this one

today.

I am regular visitor, how are you everybody?

This piece of writing posted at this website is really pleasant.

Generally I don’t read post on blogs, however I would like

to say that this write-up very pressured me to check out and do it!

Your writing taste has been surprised me. Thank you,

very nice article.

It’s very simple to find out any matter on net as compared

to textbooks, as I found this piece of writing at this

website.

Your style is really unique in comparison to other folks

I’ve read stuff from. Thank you for posting when you have the opportunity,

Guess I’ll just book mark this blog.

I don’t know if it’s just me or if everyone else experiencing problems with your blog.

It seems like some of the written text within your content are running off the screen. Can somebody

else please comment and let me know if this is happening to them too?

This might be a issue with my browser because I’ve had this happen previously.

Cheers

I like the valuable info you supply on your articles.

I’ll bookmark your blog and test again right here regularly.

I’m reasonably certain I’ll be told a lot of new stuff proper right

here! Good luck for the next!

Hmm it appears like your blog ate my first comment (it was super long)

so I guess I’ll just sum it up what I submitted and say, I’m thoroughly enjoying your blog.

I as well am an aspiring blog writer but I’m still new to the whole thing.

Do you have any tips for rookie blog writers? I’d

definitely appreciate it.