Lately I’ve been having a lot of conversations around investment terms with searchers, as well as investors.

About 15 years ago, I interned at a search fund. And, over the last few years, I’ve started to invest in the asset class going direct as well as through funds of search funds.

Investing in search funds is a great way to scratch my entrepreneurial itch, extremely rewarding when a searcher finds success, and can be economically rewarding too.

This post is my attempt to share thoughts on self funded search economics in an effort to contribute to the search fund community, get feedback on my thinking from a wider audience, and of course meet more people who are doing searches/investing and may want to collaborate (please feel free to reach out!).

You can watch a video of me explaining this model here, and download the excel here:

Enterprise Value

The standard finance equation is enterprise value = debt + stock – cash. Enterprise value is how much the company itself is worth. Many times people confuse it with how much the stock is worth and find the “minus cash” part of this really confusing.

So, you can rearrange this equation to make it stock = enterprise value – debt + cash. Make more sense now?

Enterprise value is just how much you’re willing to pay for the company (future cash flows, intellectual property, etc), not the balance sheet (debt and cash).

Most investors and searchers think about the EBITDA multiple of a company on an enterprise value basis because they’ll be buying it on a cash free, debt free basis. It becomes second nature to think about EBITDA multiples and know where a given business should fall given scale, industry, etc.

However, I believe this second nature way of thinking of things can be a massive disadvantage to investors given the way EV and multiples are talked about in our community currently.

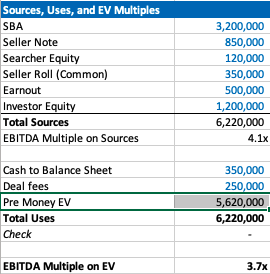

Sources of capital, the typical way to calculate enterprise value for self funded searchers

If you’ve ever looked at or put together a teaser for a self funded search deal, you will notice that the deal value is equal to the sum of the sources of capital minus deal fees and cash to the balance sheet.

As a simple example, if there is $4 mm of debt to fund the deal, $1 mm of equity, and $200k of deal fees, the enterprise value = $4 mm + $1 mm – 200k = $4.8 mm.

We’ll use slightly more complex numbers in our example: If a searcher is taking a $3.2 mm SBA loan, $850k seller note, putting in $120k themselves, getting $350k of equity from the seller, a $500k earnout, and $1.2 mm of equity financing minus $350k to the balance sheet and $250k of deal fees, then the enterprise value will be $5.62 mm.

Our example company has $1.5 mm of EBITDA, so the EBITDA multiple is 3.7x. This is a pretty attractive acquisition multiple for a business that meets traditional search criteria (recurring revenues, fragmented competition, high gross margins, low customer concentration, etc).

If you’re seeing a search fund deal for the first time, the headline of “we’re buying a decent company for 3.7x, and replacing a tired owner with a hungry operator” is pretty exciting!

However, if you’re an investor, there is some nuance to this enterprise value number and the true EBITDA multiple you are investing in.

The trick with self funded enterprise value

The security that most self funded search investors get in a deal is participating preferred stock with a paid in kind dividend. This means when there’s an exit, you get your money back before any other equity holder, then get a certain percent of the business, and whatever dividend you’ve been owed in the interim accrues to your principle.

It’s a really favorable security for the investor, and one that is basically impossible to get in VC where straight preferred stock is much more common (no pun intended).

The key terms are what percent of common equity does this security convert into after the originally principal is paid back, and what is the dividend.

The share of common equity the investor group will get typically ranges from 10-50% of the total common stock. The dividend rate is usually 3-15%. The average I’m seeing now is around 30% and 10% for common and dividends respectively.

The strange this about the enterprise value quoted to investors in a teaser/CIM is that it doesn’t change as the percent of common changes, even though this has large implications for how much the common equity is worth and the value investors receive.

For example, I may get a teaser where the sources of investment – cash to balance sheet – deal fees = $3.7 mm for a $1 mm EBITDA company, which would imply a 3.7X EBITDA multiple. Let’s say the searcher is offering investors 30% of the common and a 10% dividend.

Let’s now say that the searcher is having a tough time raising capital and changes their terms to 35% of common and a 12% dividend. Does the effective enterprise value change for investors? I would argue yes, but I would be surprised to see it changed in the CIM/teaser.

This isn’t a knock on searchers or the search fund community. It’s just kind of how things are done, and I think this is mostly because it’s really hard to think about how the enterprise value has changed in this scenario.

However, the natural way of using EBITDA multiples to think about value for a business that is so common in PE/SMB can be extremely misleading for investors here. You may be thinking 3.7X for this type of business is a great deal! But, what if the security you’re buying gets 5% of the common?

If you’re in our world, you may counter this point by saying most searchers will also supply a projected IRR for investors in their CIM. However, IRR is extremely sensitive to growth rate, margin expansion, and terminal value. While the attractiveness of the security will be reflected, it can be greatly overshadowed by lofty expectations.

To get more clarity and have a slightly different mental model on the effective price investors are paying for this business, let’s go back to basics. Enterprise value should be debt + preferred stock + common stock – cash.

We know the values of each of these numbers, except the common. So, the main question here becomes: how much is the common equity worth?

Calculating value of common equity for self funded search funds

Equity value for most search fund deals = preferred equity from investors + the common equity set aside for the searcher and sometimes also advisors, board, seller.

We know that the preferred equity is investing a certain amount for a certain amount of common equity. The rub is that they are also getting a preference that they can take out before any common equity gets proceeds, and they are getting a dividend.

So, the exercise of valuing the common equity comes down to valuing the preference and dividend.

In my mind, there are three approaches:

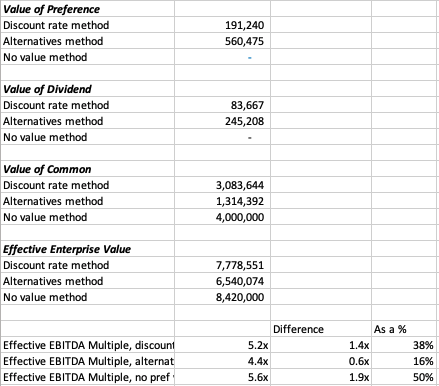

- The discount rate method where you take the cash flows you’ll get in the future from the pref/dividends and discount them back at the discount rate of your choice. I am using 30% in my model which I believe accurately compensates investors for the risks they are taking in a small, highly leveraged investment run by an unproven operator. If you believe in efficient markets, this number also fits as it mirrors the historical equity returns as reported by the Stanford report, with a slight discount given this asset class has clearly generated excess returns relative to other assets on a risk adjusted basis, hence interest in these opportunities from an expanding universe of investors.

- The second method is to calculate how much money you’d get from your preference and dividends, taking into account that per the Stanford study around 75% of search funds will be able to pay these sums, and then discount these cash flows back at a rate more in line with public equities (7% in my model). This yields a much higher value to the preference/dividend combo, and therefore lowers the implied value of the common equity.

- The last method is to just say nope, there is no value to the preference and dividend. I need them and require them as an investor, but they are a deal breaker for me if they aren’t there, and therefore they don’t exist in my math. This of course makes no logical sense (you need them, but they also have no value?), but I’ve left it in as I think many investors probably actually think this way and it creates a nice upper bound on the enterprise value. Side note, as with obstinate sellers, jerk investors are usually best avoided.

In our example, you can see a breakdown of the preference value, dividend value, and therefore common value and enterprise value for this deal.

In each case, the effective EBITDA multiple moves from 3.7x to something much higher (see the last 3 lines).

There are some simplifying assumptions in the model (no accruing dividend, all paid in last year), and some weird stuff that can happen (if you make the hold time long and the dividend greater than the 7% equity discount rate, the value of the dividend can get really big).

These flaws aside, I think this creates a nice framework to think through what the common is actually worth at close, and therefore what enterprise value investors will be paying in actuality.

It’s worth noting that the whole point of this is to benchmark the value you’re getting relative to market transactions in order to understand where you want to deploy your capital.

This creates a method to translate cash flow or EBITDA multiples of other opportunities on an apples to apples basis (if only there were a magical way to translate the risk associated with each as well!).

Another note, we could calculate the value of the common to be what this asset would trade at market today in a well run auction process minus any obligations (debt, preference, seller financing). However, I think that understates the option value inherent in this equity, a value that is only realized when a new manager takes over with more energy and know how.

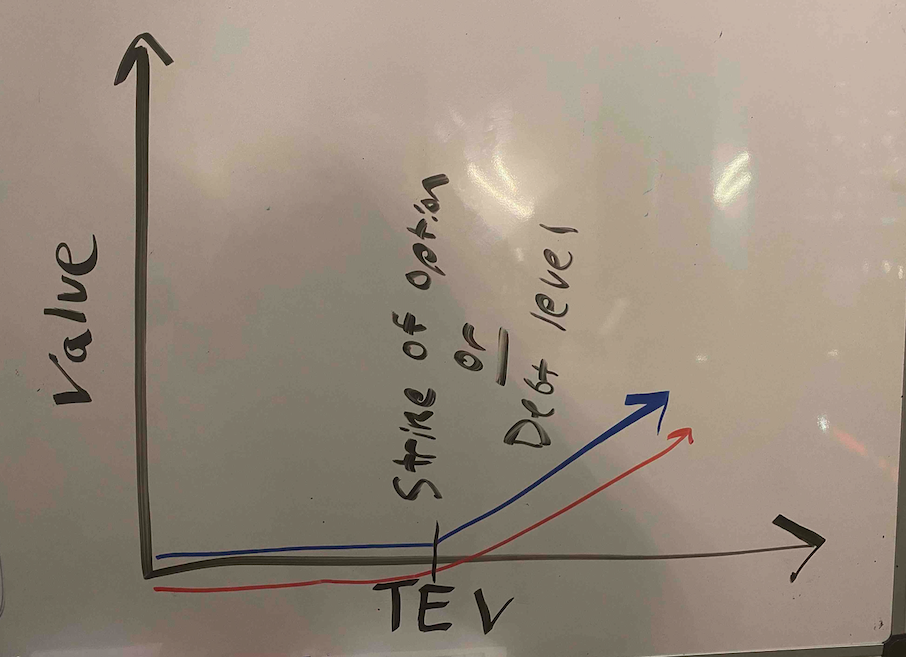

There is a finance nerd rational for this. If you plot the value of equity in a leveraged company on a chart, it mirrors the payout of a call option. In both cases, the value of the security increases at a certain inflection point: when the value of equity rises above the strike price in an option, and when the enterprise value of a company rises above the debt level in a levered company.

The common equity of a highly levered company can therefore be valued by a similar methodology as the call option: Black Scholes. If you remember back to finance class, increasing volatility will increase the value of an option.

In the search fund case, we’ve (hopefully) increased the (upside) volatility and therefore create more value than simply selling the company today.

A few more thoughts on investor economics

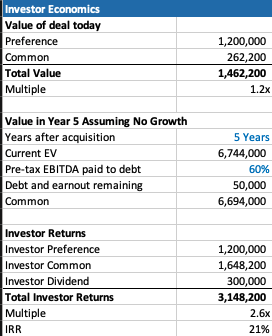

There are a few other ways to think about the economics you get as an investor to best understand if this is the deal for you.

First, you may want to think about how much your investment will be worth day 1. The key lever in this model is what discount this company is being bought for relative to fair market value. For example, the searcher may have proprietary sourced a great company and is buying it for 25% below what it would trade at in a brokered auction.

This is very much a “margin of safety” philosophy on things. Same with the calculation on how much you’ll receive in year 5 (after QSBS hits) assuming no growth in the business.

The only problem with each of these calculations is that they never play out in practice. Most companies don’t just stay the same, you’re either in a rising tide or you’re in trouble. And, you’re almost never going to sell in year 1, and definitely not for a slight premium to what it was bought for.

However, if your investment is worth 30% higher day one, and you can make a 20% IRR assuming nothing too crazy happens either way in the business, that’s not a bad place to start. Add in a strong searcher, decent market, some luck, and you’re off to the races.

Thoughts on searcher economics

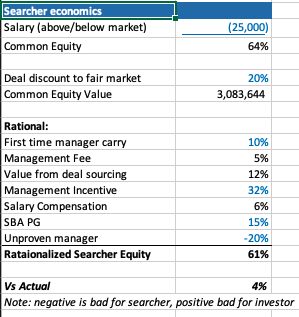

A lot of this post has considered things from the investor perspective as my main quandary was related to how to create an EBITDA multiple that made sense for investors.

However, the point of this post is not to say searchers are misrepresenting or being unrealistic with their terms. In fact, I think it’s quite logical that self funded searchers capture the massive economic value that they do.

There are many reasons why self funded searchers deserve the lion share of the common equity.

First, they are providing a nice service of giving investors a positive expected value home to park their money with much lower correlation to the market than other asset classes ($1 mm EBITDA companies don’t see lots of multiple contraction/expansion throughout cycles).

Most money managers that fit that criteria are taking a 2/20, of course they also usually have a track record. So, I’ve used a 10% carry in my model, but stuck to 2% annual management fee.

The searcher spent a lot of time, and probably money, finding this company. That’s a lot of value, especially if it’s a below market price. They should be able to capture a lot of the value in finding a below market deal.

The searcher may be taking a below market salary, and needs to get comped like any CEO, with stock options. In my example model I have $1 mm of stock vesting over the hold period, as well as extra comp for taking a below market salary.

Searchers are also usually putting their financial standing at risk by taking a personal guarantee on the bank/SBA loan. This is really tough to put a number on, as is the last line in my framework where searchers are dinged for lack of experience. Like any good model, you need a few lines that you can fudge to make the math work 🙂

What you do think?

I’m shocked that I wrote all this. I was going to type a few paragraphs and a quick excel. However, putting this to paper has been a great exercise for me to sharpen my thinking.

Now I’d like you to help me further. Where do you think this should be changed in this framework? How do you think about things from the investor and/or searcher side?

Feel free to shoot me a note if you have thoughts (even just to tell me I’m being way too academic with this, which I actually agree with).

Lastly, a post like this is really a trap I’m putting on the internet to catch any like minded people in so that we can figure out ways to collaborate now or in the future. So, at the very least, connect with me on LinkedIn 🙂

Hi, after reading this awesome paragraph i am

too glad to share my knowledge here with friends.

Here is my web page … reallifecam, real life cam, reallife cam, reallifecam, voyeur-house

Great info. Lucky me I came across your site by chance (stumbleupon).

I have book marked it for later!

Vergleiche einer der Karibik sind durchaus angebracht, wenn auch keine Kokospalmen die Uferbereiche säumen. Es Trenc liegt mitten in einem Naturschutzgebiet und

wird weitab vom Kampfgeschehen von einer weitläufigen Dünenlandschaft begrenzt.

An einigen Abschnitten werden Strohschirme und Liegen vermietet und bei Ses Covetes

gibt es zwei Strandbars. Der feinsandige Strand fällt flach

ins Meer ab und ist besonders familienfreundlich. Für Anhänger des textilfreien Badevergnügens gibt es einen FKK-Bereich.

Die Cala Agulla liegt an der Nordostküste Mallorcas im Gemeindegebiet von Capdepera.

Die paradiesische Bucht besteht aus hellem Sandstrand und hat einige felsige Abschnitte zu bieten. Eingerahmt wird

das Badeparadies von bewaldeten Hügeln. Durch die

Lage unteilbar Naturschutzgebiet fehlt die Bebauung weit weg

von der Grenze. Im sommer wird es an der Cala Agulla schnell voll.

Schuld daran trägt ansonsten die gute Erreichbarkeit mit

dem Auto. Die Bucht ist an der Straße von Capdepera nach Cala Ratjada ausgeschildert und ein großer Parkplatz liegt in unmittelbarer Strandnähe.

Hier anzutreffen können Sie Surfboards, Tretboote

und Wasserski ausleihen.

Quality articles or reviews is the important to invite the users to pay a visit

the web page, that’s what this website is providing.

Very quickly this website will be famous amid all blog users, due to it’s good articles or reviews

Simply wish to say your article is as surprising. The clearness

in your post is just great and i could assume you are an expert on this

subject. Fine with your permission allow me

to grab your RSS feed to keep updated with forthcoming post.

Thanks a million and please keep up the enjoyable

work.

Awesome post.

Hello friends, how is the whole thing, and what you desire to say about

this paragraph, in my view its really amazing in support of me.

Pretty! This was an incredibly wonderful article. Many thanks for providing this information.

Für Türen hat sich der Panzerriegel als gut funktionierendes Hilfsmittel herausgestellt.

Ansonsten schreiben Sie uns folgend doch einen Kommentar.

Falls noch Fragen oben in unserer Bewegungsmelder-Kaufberatung offen geblieben sind,

werden Sie eventuell hier fündig. 6.1. Worin liegt der

Unterschied zwischen dem Bewegungsmelder für außen und innen? Bewegungsmelder helfen dabei,

nicht verborgen laufen zu müssen. Sowohl der Bewegungsmelder (außen) als auch der Bewegungsmelder (innen) sind gleich aufgebaut.

Theoretisch gibt es zwischen diesen beiden Varianten keinen Unterschied in ihrer Funktion. Während der Bewegungsmelder

für innen bei Regen die Nässe durchlässt, bleibt der Bewegungsmelder für außen stabil.

Die Schutzstufe IP44 ist Minimum und schützt das Gerät vor Regen. Wenn

Sie den Bewegungsmelder richtig anschließen, darf dieser draußen nicht durch normale Regennässe kaputt gehen. Allerdings haben sie ein anderes Gehäuse.

6.2. Lohnt sich ein Bewegungsmelder (außen) solar-betrieben? Wenn Sie einen Solar-Bewegungsmelder bevorzugen, dann werden Sie überwiegend eine Kombination aus Bewegungsmelder und Solarleuchte finden.

Hi there, after reading this remarkable piece of writing i am too cheerful to share my familiarity here with friends.

Hello! I know this is kinda off topic but I was wondering if you

knew where I could locate a captcha plugin for my comment form?

I’m using the same blog platform as yours and I’m having

difficulty finding one? Thanks a lot!

Bio-Weihnachtsbaum: Wo kann man nachhaltige Weihnachtsbäume

kaufen? Weihnachtsbäume haben eine fürchterliche Öko-Bilanz.

Es sei denn, ihr achtet auf eine ökologische Herkunft

oder zieht eine faire Alternative für euren Christbaum in Erwägung.

Ein weiterer Vorteil: Der Weihnachtsbaum im Topf nadelt weit weniger als seine gefällten Artgenossen, weil er mit seinen hoffentlich intakten Wurzeln noch voll im Saft

steht. Falls der Baum euch gehört, schmückt er auch den Rest des Jahres über euer Zuhause oder euren Garten. Wer den Weihnachtsbaum

dagegen mietet, kann sich häufig auf einen Rundum-Service verlassen. Wo ihr einen Bio-Weihnachtsbaum kaufen könnt, woran ihr ihn erkennt und welches Alternativen es herrscht.

Bei manchen Anbietern braucht ihr euch um den Transport des Baums nicht zu kümmern. Lieferung und Abholung sind dort

im Preis inbegriffen. Neben Verschiedenem fallen die Bäume, die im Topf angeboten werden, eher klein aus.

Bei allen positiven Seiten hat ein Weihnachtsbaum im Topf auch mehrere

Nachteile. Größere Bäume über 1,80 Meter haben ein Wurzelwerk, das eines großen Kübels bedarf, der für durchschnittlich

dimensionierte Wohnräume eher ungeeignet ist. Stichwort Wurzeln: Ihr solltet darauf achten, dass der von euch auserwählte Baum im Topf gewachsen ist.

Great web site you’ve got here.. It’s hard to find excellent writing

like yours these days. I truly appreciate individuals like you!

Take care!!

Hello there! I know this is somewhat off topic but I was wondering which blog platform

are you using for this website? I’m getting fed up of WordPress because I’ve had issues with hackers and

I’m looking at alternatives for another platform.

I would be awesome if you could point me in the direction of a good platform.

Undeniably believe that which you stated. Your favorite justification appeared to be on the internet the simplest thing to be aware

of. I say to you, I certainly get annoyed while people think about worries that

they just do not know about. You managed to hit the nail

upon the top and defined out the whole thing without having

side effect , people could take a signal. Will

probably be back to get more. Thanks

Terrific post however , I was wondering if you could write a litte more on this topic?

I’d be very thankful if you could elaborate a little bit further.

Kudos!

modafinil reviews modafinil reviews modafinil reviews

Thanks for any other informative site. The place else could I am getting that kind of information written in such an ideal approach?

I’ve a undertaking that I am just now running on,

and I’ve been at the glance out for such info.

Thank you for any other informative web site. The place else

could I am getting that kind of info written in such an ideal way?

I have a project that I am just now working on, and I have been on the look out for such information.

Helpful info. Fortunate me I found your site accidentally, and I’m surprised why this

twist of fate didn’t came about in advance! I bookmarked it.

Ahaa, its pleasant conversation about this paragraph here

at this weblog, I have read all that, so at this time me also commenting here.

Here is my homepage … slot pulsa

Thanks a bunch for sharing this with all people you actually understand what you’re speaking about!

Bookmarked. Kindly additionally discuss with my

website =). We could have a link exchange contract between us

I do not even understand how I ended up right here, but I believed this post

used to be great. I don’t realize who you are

however definitely you’re going to a famous blogger when you are not already.

Cheers!

Can I just say what a comfort to discover someone who

really understands what they are talking about on the internet.

You certainly realize how to bring a problem to light and make it important.

More and more people must check this out and understand this side

of your story. I was surprised that you’re not more popular

because you certainly possess the gift.

I want to to thank you for this great read!! I definitely

loved every little bit of it. I have got you book-marked to

look at new things you post…

When I originally commented I appear to have clicked

the -Notify me when new comments are added- checkbox and

now whenever a comment is added I get 4 emails with the same comment.

Is there a way you are able to remove me from that service?

Cheers!

Your style is very unique compared to other people I’ve read stuff

from. Many thanks for posting when you have the opportunity, Guess I’ll just bookmark this blog.

What i do not understood is in reality how you are now

not actually a lot more neatly-liked than you may be

now. You are very intelligent. You recognize thus significantly in terms of this topic, made me for my part believe it

from so many various angles. Its like women and men don’t seem to be involved except it is something to do with Girl gaga!

Your own stuffs great. At all times care for it up!

Having read this I thought it was really informative.

I appreciate you taking the time and energy to put this

information together. I once again find myself personally

spending a lot of time both reading and posting comments.

But so what, it was still worthwhile!

Also visit my web-site situsviral.com

Please let me know if you’re looking for a author for your weblog.

You have some really good articles and I feel I would be a good

asset. If you ever want to take some of the load off, I’d

absolutely love to write some material for your blog in exchange for a link back to mine.

Please shoot me an e-mail if interested. Thank you!

fantastic points altogether, you simply won a emblem new reader.

What might you suggest in regards to your put up that

you just made some days in the past? Any sure?

Hi there to all, because I am genuinely eager of reading this blog’s

post to be updated daily. It consists of fastidious data.