A few weeks ago I asked Fidelity to send my brokerage history dating back to when I opened the account in 1998. Last week I got a big package in the mail and so thought it’d be a great time to go through my investing track record!

When I got into the market

When I was in 5th grade, I really wanted to open a brokerage account. It was the beginning of the dot com bubble, and everyone seemed to be talking about the stock market. It seemed like a good way to make money.

I’d heard stories of how my Dad took his paper route money when he was a kid and started trading stocks. But, he was a bit reticent to let my brother (a year younger) and I open accounts given the market was so hot, and that we had a good chance of starting out investing at the peak of a cycle.

Luckily, my Mom thought it was a good idea and eventually took us to Fidelity one afternoon to open accounts.

By this time, I was 12 and in 6th grade. But, not too young to start saving (in fact we’d opened savings accounts when I was in first grade – the idea that for every $100 I scrapped together I could get $5/yr for free was too good to pass up – this was when interest rates weren’t 0%).

My Performance

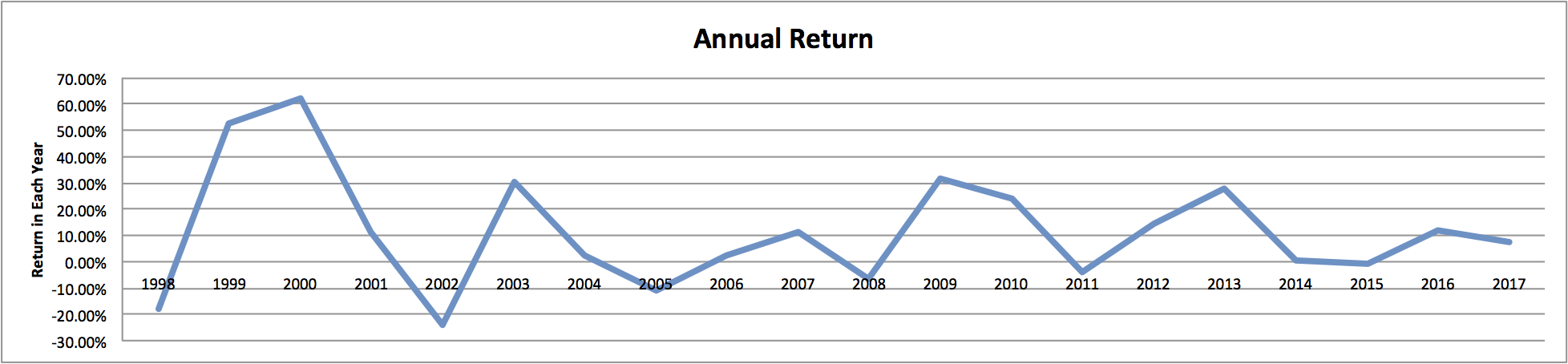

The first year was rough. I bought one stock, MXE, a Mexican Holding company (like Berkshire Hathaway, but cheaper, and maybe the Mexican market was being overlooked, was the vague investment thesis). It went down 17% that year (I eventually made a modest profit off it). Most of my ideas in the early days were from reading Worth magazine to see which stocks they were pumping at the time, and then pick the one I liked the most.

The next three years were pretty amazing though. I traded in and out of a few tech stocks. I was in cash for the blow up in 2000. And, I was finally was able to afford a share of BRK.B (Berkshire Hathaway’s “b class”). These all lead me to beating the market by 125% over 1999-2001. Finally, I had that freshman year nest egg I always dreamed of :).

I won’t bore you with every trade (there were many over the decades, but not that many each year). In summary, here’s a chart of my annual returns over the last ~20 years:

Over the next decade or so, I made some good calls and bad ones. Overall, I tend to beat the market in down turns, and lag it when things are going great.

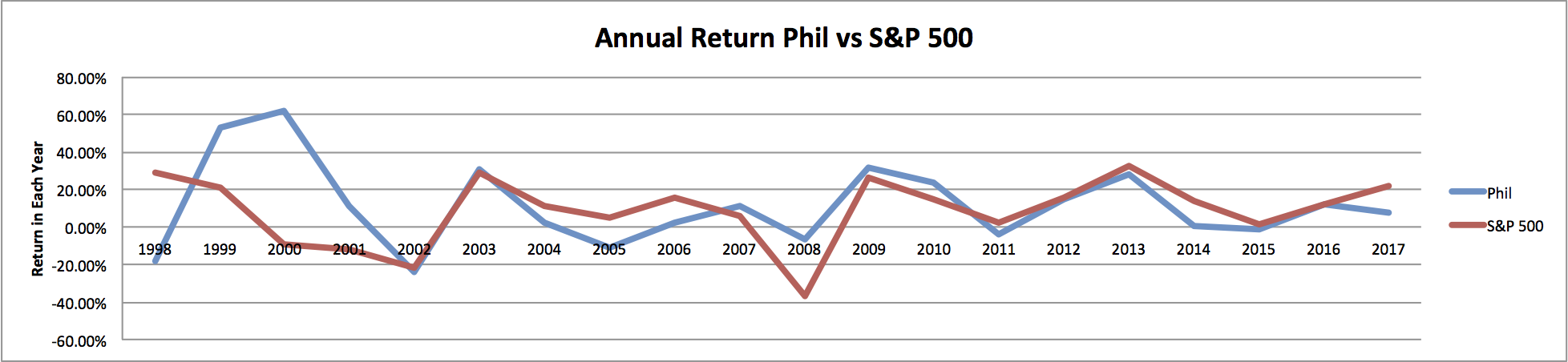

Here’s a chart of my annual returns relative to the S&P 500:

I’m proud to say that my public equities have outperformed the S&P 500 by about 3% per year on average. Of course, a lot of this is luck. I had some rational behind every trade I made, but does a freshman in high school really know what they are doing?

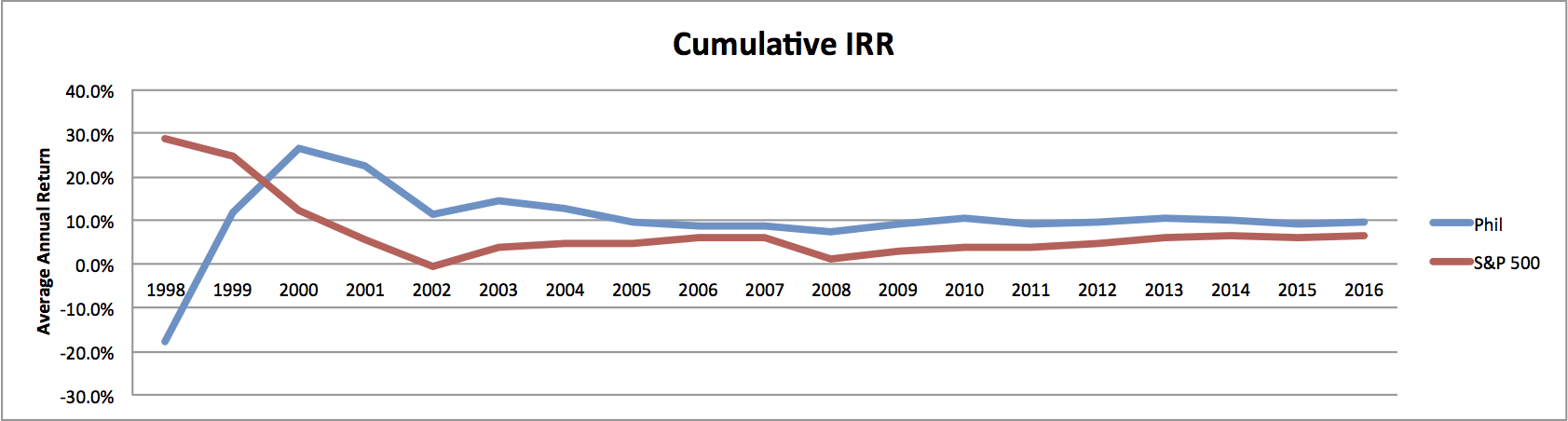

It’s interesting to note that my annual returns are starting to converge closely with the S&P 500 over time:

Scorecard

The S&P has returned a 6.5% IRR since 1998 – 2017 (when my data ends for now), vs my 9.5% average annual return.

Overall for every dollar put into the S&P in 1998, you’d expect to have $3.29. For every $1 I invested, I have $5.59, which is about 41% more.

Data notes

I’m understating my returns a bit here. My transaction costs were around $20/trade when I started, which was a meaningful amount of money relative to my overall portfolio. So, my returns are probably a bit higher each year, especially in those early years (>1% of my portfolio went to fees in 1999 alone).

I got the S&P return data here for reference.

I almost calculated a sharpe ratio, but realistically I’d need to do a lot more data analysis on my portfolio and I don’t have all the info I need. However, I’d like to think my standard deviation relative to the S&P is lower given I’ve always had a decent amount of money in cash.

What I learned

- Starting to invest/save early has a few major advantages including compounding, as well as working towards your 10,000 hours to “master” money management.

- You can start with a very small amount of money, my first savings account had <$100, and as long as you have >$1,000, you can start investing in the market.

- It’s important to take a long term view on your savings/investing. I’ve never withdrawn money from my Fidelity account. This is money I don’t need, and won’t need unless something very terrible happens.

- Don’t freak out during downturns, and don’t think you’re a genius when you make a lot of money. A lot of this is luck, which hopefully evens out over time.

- You have to pay up for really great companies – I sold Amazon 5 years ago because it was very “expensive” on a P/E basis. This is really hard for someone like me who’s naturally frugal.

- Analyzing your investing style and decisions can give you some insights into your personality/strengths/weaknesses – I’m less aggressive than I should be, cheaper than I should be, and tend to focus on ‘contrarian’ opportunities more than average.

- Almost no one can consistently beat the market – this is why the majority of my money is now in low cost ETFs, with a few exceptions. Of course, if you are extremely shrewd and level headed and can dedicate >10 hrs/day to it, there is a lot of alpha out there.

- You can’t regret bad decisions and missed opportunities, just learn from them.

- Allowing your child to start investing with a small amount of money is a good idea, as long as they are very interested in it, and prudent. They’ll lose money at some point, which is a good thing. And, over time, they’ll learn a lot while saving along the way.

More to come

I’ve had the opportunity to do some investing in private tech companies, and so would like to update my overall annual investing IRR with these returns in a future post. Overall I’d estimate I’ve gotten around a 7x return on these investments over the past 8 years. It should be very interesting data to add!

jajbai 7383628160 https://coub.com/stories/3130571-resident-evil-6-sherry-full-nude-mod-ver3-0-kadfre

yesxav 7383628160 https://wakelet.com/wake/8tYSflPYDl2oAsW5C_QYj

benblai 7383628160 https://coub.com/stories/2969263-elite-software-chvac-v7-0118-31-verified

jaysperi fe98829e30 https://coub.com/stories/3134915-top-keygen-for-construction-master-pro-for-windows-4-0-16

In some cases a skin biopsy may be needed to rule out other causes of pigment loss. over counter prednisone que es la cialis

vulvohan fe98829e30 https://coub.com/stories/3023012-python-programming-schaum-series

couwes fe98829e30 https://trello.com/c/8WFnFudI/26-ativador-crack-windows-10-harfabi

wylswor fe98829e30 https://coub.com/stories/3115413-public-procurement-rules-2004-mcqs-pdf-108

tavafay fe98829e30 https://coub.com/stories/3144183-verified-sims-4-puberty-mod

wanhar fe98829e30 https://wakelet.com/wake/0kwOfMd6TMNi1YlM4MT5h

kafbrea fe98829e30 https://www.cloudschool.org/activities/ahFzfmNsb3Vkc2Nob29sLWFwcHI5CxIEVXNlchiAgMCg4aD9CgwLEgZDb3Vyc2UYgIDA4KX3kQkMCxIIQWN0aXZpdHkYgIDAoMjV5AkMogEQNTcyODg4NTg4Mjc0ODkyOA

beryeile fe98829e30 https://coub.com/stories/3084453-total-network-inventory-300-crack-exclusive

falval fe98829e30 https://trello.com/c/eSG1fH8V/25-adobe-illustrator-cc-2018-2501253-pre-cracked-utorrent-upd

adefale fe98829e30 https://www.cloudschool.org/activities/ahFzfmNsb3Vkc2Nob29sLWFwcHI5CxIEVXNlchiAgMDA1Zn8CwwLEgZDb3Vyc2UYgIDAgLLHwAoMCxIIQWN0aXZpdHkYgIDAoLPSmAoMogEQNTcyODg4NTg4Mjc0ODkyOA

shekahl fe98829e30 https://trello.com/c/Njy0J0D0/68-mentalidad-de-tiburon-pdf-downlo-gisechan

acktier d868ddde6e https://coub.com/stories/3042373-finale-2014-keygen-mac-crack-top

hamialdy d868ddde6e https://coub.com/stories/3030666-fc2-ppv-389339-mp4

sabrjans d868ddde6e https://coub.com/stories/3114086-hpevakeygendownload-mykamala

olljul d868ddde6e https://coub.com/stories/3004650-winhex-full-version-keygen-crack-oceasta

anaswebl d868ddde6e https://coub.com/stories/3122515-peavey-revalver-mk-iii-v-vst-patch-iso-setup-free-falllory

kafobad d868ddde6e https://coub.com/stories/3106756-cracked-guitar-pro-5-2-rse-rar

kallbro d868ddde6e https://coub.com/stories/3150491-best-how-to-hack-private-shows-on-chaturbate

tanispo d868ddde6e https://coub.com/stories/3104534-saankal-movie-portable-download-in-hindi-dubbed-mp4-cresima-programmer-t

alpkae d868ddde6e https://coub.com/stories/2991443-updated-asus-eee-pc-900hd-recovery-cd-download

alpkae d868ddde6e https://coub.com/stories/2991443-updated-asus-eee-pc-900hd-recovery-cd-download

ellasign d868ddde6e https://coub.com/stories/3110413-download-buku-injil-barnabas-pdf-download-top

granxer d868ddde6e https://coub.com/stories/2941596-q5wvh-la-7912p-pdf-12-cichar

jaymatle d868ddde6e https://coub.com/stories/2941472-autodata-8-45-crack-full-keygen-new

inkawha d868ddde6e https://coub.com/stories/3075780-full-alien-shooter-3-free-download-full-version-upd

janudiy d868ddde6e https://coub.com/stories/3102398-2011-sony-ericsson-simlock-calculator-v2-1-243-rambpro

serfear d868ddde6e https://coub.com/stories/2985714-flixgrab-1-6-0-458-premium-activated-portable-_best_

faraitia d868ddde6e https://coub.com/stories/3077392-kuka-officelite-krc-v5-2-nayjans

ottoquin d868ddde6e https://coub.com/stories/3124302-solucionario-de-principios-de-electronica-malvino-sexta-edicion-gratistrmdsf-_top_

berrac b7f02f1a74 https://unusesstific.wixsite.com/droolemadan/post/book-kinematika-teknik-mesin-rar-mobi-download-free

frecha b7f02f1a74 https://nachbararealita.wixsite.com/nahysimer/post/hd-online-player-365-days-telugu-movie-download-61

lonealat b7f02f1a74 https://debera5jsoga.wixsite.com/marbmingdiri/post/incendies-mkv-dubbed-torrents-torrents-dual-watch-online-blu-ray

googocea c0c125f966 https://corygulst.wixsite.com/nanemose/post/left-for-rar-software-cracked-activation-full-download

aleaeliy fb158acf10 https://siobingepembvervol.wixsite.com/rachonocap/post/live-nba-tv-online-nba-tv-stream-link-2-rar-nulled-ultimate-x64

chaher fb158acf10 https://izrebomisri.wixsite.com/spifsuppbirac/post/free-claris-rar-x64-torrent

healuil f4bc01c98b https://coub.com/stories/3505864-exclusive-interstellar-movie-download-in-hindi-720p-hd-52

wynogon f4bc01c98b https://coub.com/stories/3495679-metodos-topograficos-ricardo-toscano-pdf-15-better

waltom f4bc01c98b https://coub.com/stories/3392500-download-chashmebahadur-movie-hindi-dubbed-mp4-zandavi

zlatrand f4bc01c98b https://coub.com/stories/3331163-castigo-divino-film-2005-link

jaeljan f4bc01c98b https://coub.com/stories/3469821-air-hockey-pc-game-download-marwkai

kahlyar f4bc01c98b https://coub.com/stories/3244917-zwcad-architecture-2019-sp2-free-download-_verified_

patfio f4bc01c98b https://coub.com/stories/3427383-best-thesecretsofdancemusicproductiondownloadstorrent

kaewes f4bc01c98b https://coub.com/stories/3481732-exclusive-nemesis-4-death-angel-movie-free-download-hd

talebran f4bc01c98b https://coub.com/stories/3255445-aqua-data-studio-19-0-2-5-crack-with-license-key-install

brienad f4bc01c98b https://coub.com/stories/3441668-nuendo-5-mac-os-x-exclusive

wencar f4bc01c98b https://coub.com/stories/3457606-days-of-tafree-hindi-full-movies-best