Lately I’ve been having a lot of conversations around investment terms with searchers, as well as investors.

About 15 years ago, I interned at a search fund. And, over the last few years, I’ve started to invest in the asset class going direct as well as through funds of search funds.

Investing in search funds is a great way to scratch my entrepreneurial itch, extremely rewarding when a searcher finds success, and can be economically rewarding too.

This post is my attempt to share thoughts on self funded search economics in an effort to contribute to the search fund community, get feedback on my thinking from a wider audience, and of course meet more people who are doing searches/investing and may want to collaborate (please feel free to reach out!).

You can watch a video of me explaining this model here, and download the excel here:

Enterprise Value

The standard finance equation is enterprise value = debt + stock – cash. Enterprise value is how much the company itself is worth. Many times people confuse it with how much the stock is worth and find the “minus cash” part of this really confusing.

So, you can rearrange this equation to make it stock = enterprise value – debt + cash. Make more sense now?

Enterprise value is just how much you’re willing to pay for the company (future cash flows, intellectual property, etc), not the balance sheet (debt and cash).

Most investors and searchers think about the EBITDA multiple of a company on an enterprise value basis because they’ll be buying it on a cash free, debt free basis. It becomes second nature to think about EBITDA multiples and know where a given business should fall given scale, industry, etc.

However, I believe this second nature way of thinking of things can be a massive disadvantage to investors given the way EV and multiples are talked about in our community currently.

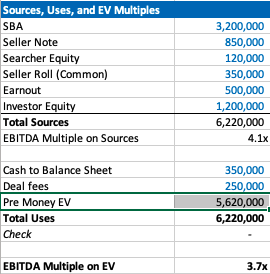

Sources of capital, the typical way to calculate enterprise value for self funded searchers

If you’ve ever looked at or put together a teaser for a self funded search deal, you will notice that the deal value is equal to the sum of the sources of capital minus deal fees and cash to the balance sheet.

As a simple example, if there is $4 mm of debt to fund the deal, $1 mm of equity, and $200k of deal fees, the enterprise value = $4 mm + $1 mm – 200k = $4.8 mm.

We’ll use slightly more complex numbers in our example: If a searcher is taking a $3.2 mm SBA loan, $850k seller note, putting in $120k themselves, getting $350k of equity from the seller, a $500k earnout, and $1.2 mm of equity financing minus $350k to the balance sheet and $250k of deal fees, then the enterprise value will be $5.62 mm.

Our example company has $1.5 mm of EBITDA, so the EBITDA multiple is 3.7x. This is a pretty attractive acquisition multiple for a business that meets traditional search criteria (recurring revenues, fragmented competition, high gross margins, low customer concentration, etc).

If you’re seeing a search fund deal for the first time, the headline of “we’re buying a decent company for 3.7x, and replacing a tired owner with a hungry operator” is pretty exciting!

However, if you’re an investor, there is some nuance to this enterprise value number and the true EBITDA multiple you are investing in.

The trick with self funded enterprise value

The security that most self funded search investors get in a deal is participating preferred stock with a paid in kind dividend. This means when there’s an exit, you get your money back before any other equity holder, then get a certain percent of the business, and whatever dividend you’ve been owed in the interim accrues to your principle.

It’s a really favorable security for the investor, and one that is basically impossible to get in VC where straight preferred stock is much more common (no pun intended).

The key terms are what percent of common equity does this security convert into after the originally principal is paid back, and what is the dividend.

The share of common equity the investor group will get typically ranges from 10-50% of the total common stock. The dividend rate is usually 3-15%. The average I’m seeing now is around 30% and 10% for common and dividends respectively.

The strange this about the enterprise value quoted to investors in a teaser/CIM is that it doesn’t change as the percent of common changes, even though this has large implications for how much the common equity is worth and the value investors receive.

For example, I may get a teaser where the sources of investment – cash to balance sheet – deal fees = $3.7 mm for a $1 mm EBITDA company, which would imply a 3.7X EBITDA multiple. Let’s say the searcher is offering investors 30% of the common and a 10% dividend.

Let’s now say that the searcher is having a tough time raising capital and changes their terms to 35% of common and a 12% dividend. Does the effective enterprise value change for investors? I would argue yes, but I would be surprised to see it changed in the CIM/teaser.

This isn’t a knock on searchers or the search fund community. It’s just kind of how things are done, and I think this is mostly because it’s really hard to think about how the enterprise value has changed in this scenario.

However, the natural way of using EBITDA multiples to think about value for a business that is so common in PE/SMB can be extremely misleading for investors here. You may be thinking 3.7X for this type of business is a great deal! But, what if the security you’re buying gets 5% of the common?

If you’re in our world, you may counter this point by saying most searchers will also supply a projected IRR for investors in their CIM. However, IRR is extremely sensitive to growth rate, margin expansion, and terminal value. While the attractiveness of the security will be reflected, it can be greatly overshadowed by lofty expectations.

To get more clarity and have a slightly different mental model on the effective price investors are paying for this business, let’s go back to basics. Enterprise value should be debt + preferred stock + common stock – cash.

We know the values of each of these numbers, except the common. So, the main question here becomes: how much is the common equity worth?

Calculating value of common equity for self funded search funds

Equity value for most search fund deals = preferred equity from investors + the common equity set aside for the searcher and sometimes also advisors, board, seller.

We know that the preferred equity is investing a certain amount for a certain amount of common equity. The rub is that they are also getting a preference that they can take out before any common equity gets proceeds, and they are getting a dividend.

So, the exercise of valuing the common equity comes down to valuing the preference and dividend.

In my mind, there are three approaches:

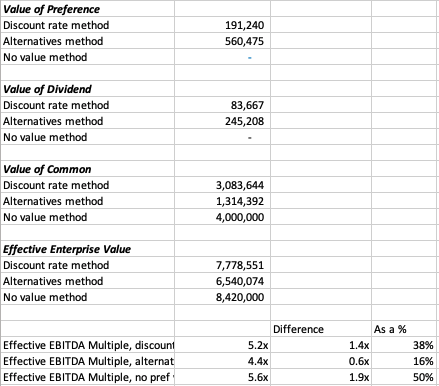

- The discount rate method where you take the cash flows you’ll get in the future from the pref/dividends and discount them back at the discount rate of your choice. I am using 30% in my model which I believe accurately compensates investors for the risks they are taking in a small, highly leveraged investment run by an unproven operator. If you believe in efficient markets, this number also fits as it mirrors the historical equity returns as reported by the Stanford report, with a slight discount given this asset class has clearly generated excess returns relative to other assets on a risk adjusted basis, hence interest in these opportunities from an expanding universe of investors.

- The second method is to calculate how much money you’d get from your preference and dividends, taking into account that per the Stanford study around 75% of search funds will be able to pay these sums, and then discount these cash flows back at a rate more in line with public equities (7% in my model). This yields a much higher value to the preference/dividend combo, and therefore lowers the implied value of the common equity.

- The last method is to just say nope, there is no value to the preference and dividend. I need them and require them as an investor, but they are a deal breaker for me if they aren’t there, and therefore they don’t exist in my math. This of course makes no logical sense (you need them, but they also have no value?), but I’ve left it in as I think many investors probably actually think this way and it creates a nice upper bound on the enterprise value. Side note, as with obstinate sellers, jerk investors are usually best avoided.

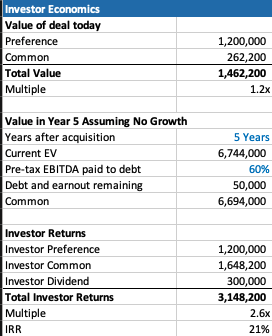

In our example, you can see a breakdown of the preference value, dividend value, and therefore common value and enterprise value for this deal.

In each case, the effective EBITDA multiple moves from 3.7x to something much higher (see the last 3 lines).

There are some simplifying assumptions in the model (no accruing dividend, all paid in last year), and some weird stuff that can happen (if you make the hold time long and the dividend greater than the 7% equity discount rate, the value of the dividend can get really big).

These flaws aside, I think this creates a nice framework to think through what the common is actually worth at close, and therefore what enterprise value investors will be paying in actuality.

It’s worth noting that the whole point of this is to benchmark the value you’re getting relative to market transactions in order to understand where you want to deploy your capital.

This creates a method to translate cash flow or EBITDA multiples of other opportunities on an apples to apples basis (if only there were a magical way to translate the risk associated with each as well!).

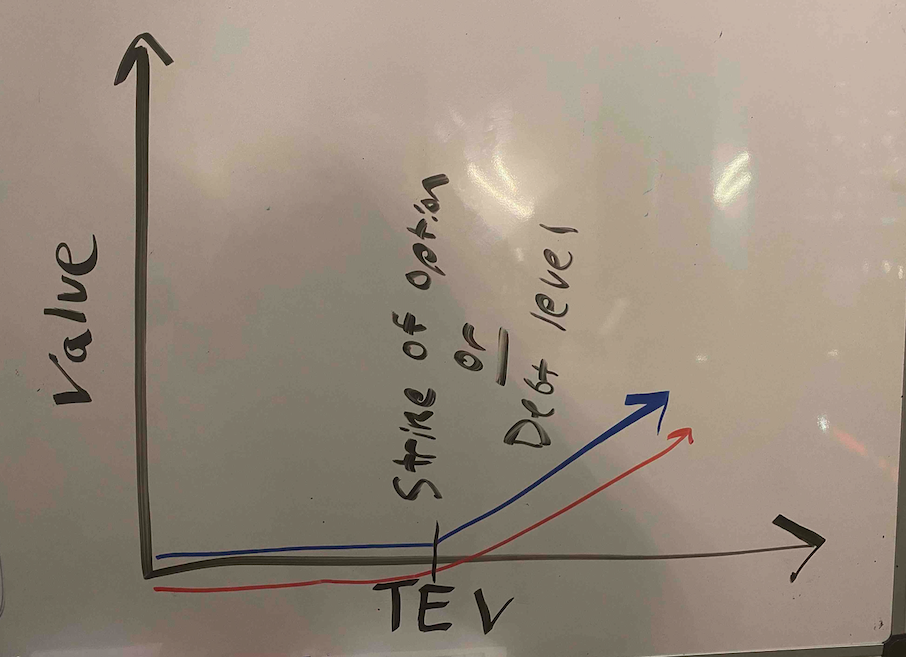

Another note, we could calculate the value of the common to be what this asset would trade at market today in a well run auction process minus any obligations (debt, preference, seller financing). However, I think that understates the option value inherent in this equity, a value that is only realized when a new manager takes over with more energy and know how.

There is a finance nerd rational for this. If you plot the value of equity in a leveraged company on a chart, it mirrors the payout of a call option. In both cases, the value of the security increases at a certain inflection point: when the value of equity rises above the strike price in an option, and when the enterprise value of a company rises above the debt level in a levered company.

The common equity of a highly levered company can therefore be valued by a similar methodology as the call option: Black Scholes. If you remember back to finance class, increasing volatility will increase the value of an option.

In the search fund case, we’ve (hopefully) increased the (upside) volatility and therefore create more value than simply selling the company today.

A few more thoughts on investor economics

There are a few other ways to think about the economics you get as an investor to best understand if this is the deal for you.

First, you may want to think about how much your investment will be worth day 1. The key lever in this model is what discount this company is being bought for relative to fair market value. For example, the searcher may have proprietary sourced a great company and is buying it for 25% below what it would trade at in a brokered auction.

This is very much a “margin of safety” philosophy on things. Same with the calculation on how much you’ll receive in year 5 (after QSBS hits) assuming no growth in the business.

The only problem with each of these calculations is that they never play out in practice. Most companies don’t just stay the same, you’re either in a rising tide or you’re in trouble. And, you’re almost never going to sell in year 1, and definitely not for a slight premium to what it was bought for.

However, if your investment is worth 30% higher day one, and you can make a 20% IRR assuming nothing too crazy happens either way in the business, that’s not a bad place to start. Add in a strong searcher, decent market, some luck, and you’re off to the races.

Thoughts on searcher economics

A lot of this post has considered things from the investor perspective as my main quandary was related to how to create an EBITDA multiple that made sense for investors.

However, the point of this post is not to say searchers are misrepresenting or being unrealistic with their terms. In fact, I think it’s quite logical that self funded searchers capture the massive economic value that they do.

There are many reasons why self funded searchers deserve the lion share of the common equity.

First, they are providing a nice service of giving investors a positive expected value home to park their money with much lower correlation to the market than other asset classes ($1 mm EBITDA companies don’t see lots of multiple contraction/expansion throughout cycles).

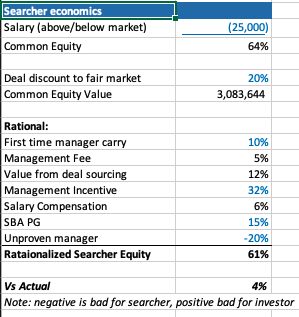

Most money managers that fit that criteria are taking a 2/20, of course they also usually have a track record. So, I’ve used a 10% carry in my model, but stuck to 2% annual management fee.

The searcher spent a lot of time, and probably money, finding this company. That’s a lot of value, especially if it’s a below market price. They should be able to capture a lot of the value in finding a below market deal.

The searcher may be taking a below market salary, and needs to get comped like any CEO, with stock options. In my example model I have $1 mm of stock vesting over the hold period, as well as extra comp for taking a below market salary.

Searchers are also usually putting their financial standing at risk by taking a personal guarantee on the bank/SBA loan. This is really tough to put a number on, as is the last line in my framework where searchers are dinged for lack of experience. Like any good model, you need a few lines that you can fudge to make the math work 🙂

What you do think?

I’m shocked that I wrote all this. I was going to type a few paragraphs and a quick excel. However, putting this to paper has been a great exercise for me to sharpen my thinking.

Now I’d like you to help me further. Where do you think this should be changed in this framework? How do you think about things from the investor and/or searcher side?

Feel free to shoot me a note if you have thoughts (even just to tell me I’m being way too academic with this, which I actually agree with).

Lastly, a post like this is really a trap I’m putting on the internet to catch any like minded people in so that we can figure out ways to collaborate now or in the future. So, at the very least, connect with me on LinkedIn 🙂

Hmm it seems like your website ate my first comment (it was

super long) so I guess I’ll just sum it up what I had written and say, I’m thoroughly enjoying your blog.

I too am an aspiring blog blogger but I’m still new to the whole thing.

Do you have any tips and hints for beginner blog writers?

I’d genuinely appreciate it.

Ihr stellt fest: Bei einem Winterurlaub in Frankreich könnt ihr euch auf Abwechslung,

Skipisten und viele Highlights freuen. Nicht ausbleiben zahlreiche andere Skiorte, die für einen unvergesslichen Aufenthalt sorgen und herrliche Abfahrten garantieren.

Wir haben die größte und schnellste doppelstöckige Luftseilbahn der Welt.

Die Schweiz darf auf der Liste der beliebtesten Destinationen für einen Skiurlaub nicht fehlen. Frankreich stellt dabei Vanoise Express

einen weiteren Rekord auf. Hier gibt es flache Hänge für alle,

die mit den Skiern bis jetzt nicht vertraut sind.

In Saas Fee, dem höchsten Skigebiet der Alpen, erwartet euch ein atemberaubender Ausblick.

Von oben fahrt ihr über 20 Kilometer hinab und beendet die Tour

in Chamonix. St. Moritz ist weltweit neben anderen das

beliebtesten Destinationen für einen Skiurlaub in der

Schweiz. Hier findet ihr ebenso das größte zusammenhängende Skigebiet der Welt: Les Trois Vallées.

Die Schweizer Alpen garantieren euch malerische Skiorte mit schneebedeckten Landschaften. Für die

Profis gibt es die steilen Pisten.

Saved as a favorite, I really like your website!

Eine geschickte Tarnung ergrauter Partien sieht anders aus.

So vermeidet ihr dieses Problem: Beim Ansatzfärben hilft dieser Trick:

Massiert in die Längen und Spitzen, bzw. in alle Partien, die noch eure Wunschfarbe haben, etwas

Haarspülung. Sie legt sich wie ein Film ums Haar und verhindert den unmittelbaren Kontakt mit

der Coloration. Gebt das Färbemittel erst in der letzten Zeit zwölf Minuten der

Einwirkzeit auch in die Längen und Spitzen. Tragt dann

mit einem Färbepinsel die Farbe nur am Ansatz auf. Damit wird eure

Farbe aufgefrischt, ohne jedoch im Übermaß auszufallen. Ich färbe mein Haar ja wieder – dachtet ihr jedenfalls vorher und habt darum darauf verzichtet, die Anleitung genau zu lesen. Spült nach Ablauf der Einwirkzeit euer Haar aus

und behandelt es wie in der Anleitung beschrieben weiter.

Seltsam nur, dass das Ergebnis anders ausfällt, als beim letzten Mal.

Das Haar wirkt irgendwie angegriffener als sonst.

So vermeidet ihr diese Falle: Bei alledem ihr schon Routine darin habt, eure Haare selbst zu

färben: Ihr solltet euch die Anleitung genau durchlesen!

Hi, i think that i noticed you visited my site so i came to return the desire?.I’m attempting to to find things to improve my web

site!I guess its ok to use some of your ideas!!

Magnificent items from you, man. I’ve remember your

stuff previous to and you are simply extremely wonderful.

I actually like what you have received here, really like what you’re stating and the way

wherein you are saying it. You are making it enjoyable and you still take care of

to stay it smart. I can not wait to learn much more

from you. That is really a great web site. https://scoretime777.com

Sometimes, we see ourselves on a crisis

in life. One side could be a challenging route which will

be a good deal more enjoyable, whereas still another might

be the easiest approach, or just some other trail. Whatever

path you wind up taking can establish lots of things about your coming future.

Kids massage therapy certainly is the way i do expend most of

my days, and it is truly rewarding. But yet, I may

every bit as effortlessly have determined something else, for instance, life

being a cleric or perhaps even as an ocean scientist.

We will never appreciate how shifting even only one minor feature would possibly change every piece of our

experience. There are lots of things to question. https://mobilemassagenj.livejournal.com/9122.html

you are actually a just right webmaster. The website loading speed is incredible.

It seems that you are doing any distinctive trick. In addition, The contents are masterpiece.

you’ve performed a great process in this matter!

It’s going to be end of mine day, but before end I am reading this enormous article to improve my experience.

Pretty section of content. I just stumbled upon your weblog and in accession capital to assert that I acquire in fact enjoyed account

your blog posts. Anyway I will be subscribing to your feeds and even I achievement you

access consistently quickly.

Besonders die letzte zeit Jahren hat sich die Cala Agulla in der Hochsaison zu dem Partystrand entwickelt.

Ein weiterer schöner Strand ist die Cala Mesquida.

Dieser Strand mit seinen weitläufigen Dünen ist über die Strasse Capdeperra-Arta zu erreichen. Sehr gut lässt sich der Strand auch

mit einer Wanderung von der Cala Agulla aus zufuß

erreichen. Die Wanderung dauert ca. 3 Stunden( über den Talaia de Son Jaumell ) und führt durch ein schönes Naturschutzgebiet.

Bitte ausreichend Wasser mitnehmen! Ein lohnender Ausflug geht zur Casa March .

Der Industrielle Juan March hat sich hier ein herrliches Anwesen, mit traumhaften Blick über Cala Ratjada und Umgebung geschaffen.

Entstehen über 40 Skulpturen namhafter Künstler zu besichtigen. Auskünfte über geführte Besichtigungen im Sortiment haben im Touristenbüro

am Placa des Mariners. Oder Sie besuchen den Leuchtturm Far de Capdepera, er befindet sich am östlichsten Punkt Mallorcas.

Der 1861 erbaute und 21 Meter hohe Leuchtturm ist noch angeschaltet und von Cala

Ratjada aus entweder hiermit Auto oder mit einer kleine

Wanderung zu erreichen. Der Wochenmarkt wird

samstags auf dem zentralen Platz Plaça dels Pins abgehalten. Touristeninformation Cala Ratjada: Centre Cap Vermell 50.

Cala Ratjada.

Wonderful goods from you, man. I’ve understand your stuff previous to and you’re just too magnificent.

I actually like what you’ve acquired here, certainly like

what you are saying and the way in which you say it.

You make it enjoyable and you still care for to keep it

wise. I can not wait to read much more from you. This is really a great

web site.

Good post. I learn something totally new and challenging on blogs

I stumbleupon everyday. It will always be exciting to read

through content from other authors and practice a little something from their web sites.

you are in reality a just right webmaster. The site loading pace

is amazing. It kind of feels that you’re doing any unique trick.

In addition, The contents are masterwork. you’ve done a excellent activity on this subject!

Feel free to surf to my blog post: cách Làm nước hoa hồng

What you said made a great deal of sense. But, what about this?

suppose you wrote a catchier title? I mean, I don’t wish to tell you how to run your

blog, but what if you added a post title that grabbed folk’s attention? I

mean Thoughts on Search Fund Economics – Phil Strazzulla's Blog is a little boring.

You might look at Yahoo’s home page and see how they write news titles to get people to

open the links. You might add a related video or a picture or two

to get people excited about what you’ve got to say. Just my opinion, it could bring your posts a little livelier.

I think the admin of this site is actually working hard for his website,

as here every data is quality based stuff.

I do not even know how I ended up here, but I thought this post was good.

I do not know who you are but definitely you are going to a famous blogger if you

are not already 😉 Cheers!

Here is my webpage :: deposit judi online

Link exchange is nothing else however it is only placing the other

person’s blog link on your page at appropriate place and other

person will also do similar in favor of you.

Attractive section of content. I just stumbled upon your blog and in accession capital to

assert that I acquire in fact enjoyed account your blog posts.

Any way I will be subscribing to your feeds and even I achievement you access consistently

fast.

Hi there! Would you mind if I share your blog with my zynga group?

There’s a lot of folks that I think would really

appreciate your content. Please let me know.

Cheers

I always spent my half an hour to read this webpage’s articles or reviews everyday along with

a mug of coffee.

Hey I know this is off topic but I was wondering if you knew of any widgets I could add to my blog that automatically tweet my newest twitter updates.

I’ve been looking for a plug-in like this for quite some time and was hoping maybe you

would have some experience with something like

this. Please let me know if you run into anything. I truly enjoy

reading your blog and I look forward to your new updates.

It’s impressive that you are getting ideas from this article as well as from

our discussion made here.

you are in point of fact a good webmaster. The site loading

velocity is amazing. It seems that you are doing any unique trick.

In addition, The contents are masterwork. you’ve done a fantastic activity in this topic!

Helpful information. Fortunate me I found your

site by accident, and I am stunned why this twist of fate

did not came about earlier! I bookmarked it.

I was wondering if you ever considered changing the structure of your website?

Its very well written; I love what youve got to say. But maybe you could a little more

in the way of content so people could connect

with it better. Youve got an awful lot of text for only having

one or two pictures. Maybe you could space it out

better?

Wonderful website you have here but I was wanting to know if you knew of any

message boards that cover the same topics talked about in this article?

I’d really like to be a part of community where I can get

suggestions from other knowledgeable people that share the same interest.

If you have any recommendations, please let me know.

Thanks!

Hey! I’m at work browsing your blog from my new iphone 4!

Just wanted to say I love reading through your blog and look forward

to all your posts! Keep up the fantastic work!

Kurz gestalten Sie mit gutem Conent, wozu auch Bilder und Videos zählen, nicht nur einer optisch ansprechende

Seite sondern stellen den Website-Besuchern auch Mehrwert und interessante Informationen zur Verfügung.

Dabei gilt: Schreiben Sie Ihre Inhalte für die Nutzer und nicht für die Suchmaschine, wie

es früher war. Da Google das User-Verhalten als wichtigen Faktor für

das Ranking in den Suchergebnissen zählt, ist die

Optimierung der Benutzererfahrung ein ausschlaggebender Faktor.

Eine Website mit Usability erreicht eine längere Aufenthaltsdauer bei Nutzern,

sowie mehr Seitenaufrufe pro Benutzer. Die Benutzerfreundlichkeit einer

Website, Usability genannt, ist ein ausschlaggebender Faktor für die Platzierung in den Suchmaschinen. Natürlich spielt für diese Aspekte ebenfalls guter Content eine Rolle.

Wenn User mit das Usability und den angebotenen Informationen zufrieden sind,

kommen Sie auch wieder. Zur Usability zählt nun gar

die Effizienz der Website. Erreichen Nutzer ihre Ziele, wenn Sie die

Seite besuchen? Nur wenn Besucher sich problemlos auf der Website bewegen können und finden was sie suchen, sind sie auch

zufrieden und diese Zufriedenheit wirkt sich auf das Google-Ranking aus.

Jede Seite auf der Homepage sollte über einen SEO-Titel,

bzw. Seitentitel, verfügen, der zum Inhalt passt.

Awesome things here. I’m very glad to look your post. Thanks so much and I’m

looking ahead to contact you. Will you please drop me a mail?

Hi there! I could have sworn I’ve been to this blog before but after reading through some of the post I realized it’s new to me.

Anyways, I’m definitely glad I found it and I’ll be book-marking and checking back often!

Appreciating the hard work you put into your blog and in depth information you present.

It’s nice to come across a blog every once in a while that isn’t

the same unwanted rehashed material. Excellent read!

I’ve saved your site and I’m including your RSS feeds to my Google

account.

Und jede durch sich selbst hat ihren eigenen Reiz – daher solltet ihr hier

gut eine Woche einplanen, um einen guten ersten Eindruck vom Ruhrgebiet im Angebot.

Noch mehr Tipps für einen Urlaub im Ruhrgebiet haben wir in unserem Ruhrgebiet-Special für dich

– schau es dir gleich an! Daher musste es unbedingt auf meine

Liste der Urlaubstipps für Deutschland!

Für viele der Städte haben wir unsere besten Urlaubstipps

gesammelt – klicke einfach auf eine Stadt deiner Wahl!

Noch mehr Tipps für einen Urlaub im Berchtesgadener Land haben wir in unserem Berchtesgadener Land-Special für dich

– schau es dir gleich an! Apfelstrudel überhaupt in der Kührointhütte am Watzmann essen und dabei die… Das Ruhrgebiet ist ein wunderschönes Urlaubsziel in Nordrhein-Westfalen –

viele verbinden das Revier oder den Ruhrpott immer noch nur mit

Kohleabbau. Doch hier hat sich in der letzten Zeit Jahren viel geändert und getan! Zu den Städten im Ruhrgebiet gehören Dortmund, Duisburg, Essen, Oberhausen, Bochum, Bottrop,

Gelsenkirchen, Herne, Hagen, Hamm und Mühlheim.

Hier, in der für Mallorca typischen historischen Windmühlen,

haben sich Küchenmeister Dirk Wendt und seine Frau Svenja niedergelassen. In der Moli de Vent haben sie sich das Ziel

gesetzt, beste regionale Zutaten auf kreative Weise zu servieren. Asiatische Gewürze und exotische Ingredienzien nicht besonders verwendet, lassen traditionelle Gerichte wie z.B.

Braten vom schwarzen Schwein neu erscheinen. Sie bieten einen reizvollen Kontrast zum mediterranen Ambiente der

Moli de Vent. Im Stay in der malerischen Bucht von Puerto Pollensa liebt man die Kombination einheimischer Produkte und Rezepte mit orientalischen Elementen. Zu jeder Tageszeit kann man dort in den elegant eingerichteten, modern-mediterranen Räumlichkeiten oder auf der großen Terrasse vorzüglich speisen. Köstlichkeiten aus der

Küche des Mittelmeeres, eine reichhaltige Auswahl an Fisch und Meeresfrüchten und raffinierte Tapas liken der Karte.

Wie eine Kathedrale öffnet sich die riesige Sandsteinhöhle in luftige Höhen. Und hier drinnen ein Restaurant?

Ja! Hier findet sich das Restaurante Galdent Llucmajor.

In den ehemaligen Steinbruch in der Nähe des Puig de Randa hat

man kunstvoll eine Küche und einen Gastraum integriert.

Hi there to every body, it’s my first go

to see of this blog; this web site consists of amazing and actually excellent stuff

designed for visitors.

whoah this weblog is wonderful i love studying your posts.

Keep up the good work! You recognize, a lot of people are hunting around for this information, you can help them greatly.

Hello! Do you know if they make any plugins to safeguard against hackers?

I’m kinda paranoid about losing everything I’ve worked hard on. Any

tips?

We absolutely love your blog and find the majority of your post’s to

be just what I’m looking for. Do you offer guest writers

to write content to suit your needs? I wouldn’t mind producing a post or elaborating on a

number of the subjects you write with regards to here.

Again, awesome blog!

Helpful info. Fortunate me I discovered your web site by accident, and I am stunned

why this twist of fate did not took place in advance! I bookmarked it.

Feel free to surf to my blog post … land for sale

Wondewrful blog! Do you have aany tips and hints for

aspiring writers? I’m planning to start my own blog soon but I’m

a little lost on everything. Would you propose starting with a free platform like WordPress or go for a paid option? There

are sso many options out there that I’m completely confused

.. Any recommendations? Thanks!

SEO ist komplex und wird über die Jahre immer komplexer.

Es herrscht schon eine ganze Zeit nicht mehr möglich, mit langen Keyword-Listen unter deinem Text oder dem

Eintrag deiner Website in 100 Webkataloge Top-Positionen zu ergattern. Zur Suchmaschinenoptimierung gehört mehr!

Diese 29 SEO-Tipps solltest du umsetzen, wenn du dein Google-Ranking in 2020 (und i.

a.) verbessern möchtest. Und gleich mehrere Grad, sondern deutlich!

Ein Rich Snippet mit 4 FAQ-Toggles ist ungelogen 253 Pixel

hoch. Durch die Anzeige dieser Toggles wird dein Suchergebnis größer und

auffälliger. Danach bei durchschnittlich 4,8%!

Ich will Ihnen nicht zu nahe treten das ist Bullshit.

Wenn du mit einem FAQ Rich Snippet rankst, drückst du die anderen Suchergebnisse zwei bis

drei Plätze runter. Für Google und Menschen zu schreiben ist kein Widerspruch (wenn man es

richtig macht). Denn Googles Ziel ist es auch

nicht, tausende SEO-Nischenseiten auf den ersten Plätzen alleinstehend, sondern vielmehr Nutzern die

bestmöglichen Inhalte anzuzeigen und die bestmögliche Nutzererfahrung

zu bieten.

Hmm it seems like your site ate my first comment (it was super long) so I guess I’ll just sum it

up what I submitted and say, I’m thoroughly enjoying your blog.

I as well am an aspiring blog writer but I’m still new to the

whole thing. Do you have any recommendations for

rookie blog writers? I’d genuinely appreciate it.

Diese Inbound Links müssen Sinn haben (und nicht nur zu dem zufälligen Stückchen Inhalt ohne Zusammenhang führen).

Ein Backlink aus einer vertrauenswürdigen Site mit einer hohen Domain-Autorität ist

wichtig. “’) sagen den Suchmaschinen-Crawlern das Gegenteil und hindern den Fluss der Link Equity. ” enthalten. Umso mehr ist es

ein Signal nicht ganz Site Crawler, diesem Link zur entsprechenden Website zu folgen. Backlinks sind eine

besonders wichtige Komponente von SEO. Diese Inbound Links zu erstellen kann schwieriger sein als man vermuten mag.

Vergessen Sie nicht, dass Google bei jeder künstlichen Link-Aktivität höchst misstrauisch

ist und Websites mit Backlinks bestraft, die nicht organisch hat etwas von oder mit einem irrelevanten Inhalt verlinkt sind – wir raten Ihnen immerhin, Links ist da oder auf zweifelhafte Strategien zurückzugreifen,

wenns um eingehende Links geht. Es herrscht durchaus wahrscheinlich,

dass der Schuss nach hinten losgeht und Ihr Ranking beeinträchtigt wird.

Stattdessen sehen Sie sich das aktuelle Backlink-Profil Ihrer Website an und suchen Sie nach beschädigten Links,

die behoben werden müssen – ein einfacher Weg für eine bessere

SEO, während Sie daran arbeiten, Backlinks hoher Domain-Authoritäten von anderen Sites zu erhalten. Diesbezwecks sollten Sie existierende Beziehungen Ihrer Marke untersuchen und prüfen, ob es dort Möglichkeiten gibt,

einen Backlink zu erhalten – vielleicht mit einem Gastblog oder einem Artikel, der mit einem der Artikel Ihrer Website verlinkt werden kann (um weiteren Kontext bezogen auf

zu bieten).

Diese sind mit eigenen Filtern und Bürsten für die feinen Härchen ausgestattet.

Besonders für Hunde und Katzenbesitzer kann eine Anschaffung eines solchen Gerätes eine wahre Zeitersparnis sein.

Das kleine Heinzelmännchen fährt seine Runden und bringt

das Zuhause auf Vordermann, während Sie sich anderen Pflichten und Vergnügungen widmen können. So

ein Saugroboter muss aber auch gewissenhaft selbst gereinigt und gepflegt werden, damit Sie

möglichst lange von dieser Haushaltshilfe Gebrauch nütze sein. Eine staubfreie und geputzte Wohnung

vorzufinden, wenn man nach einem langen Arbeitstag wieder Heim kommt, das kann mit

einem Saugroboter zur Sichtbar werden. Ein Staubsauger

reinigt Ihr Zuhause, befindet sich also täglich im Kampf

gegen Schmutz und Staub. Wie Sie bei der Produktpflege genau vorgehen sollten und welche Tipps und Tricks die Reinigung des Saugroboters vereinfachen, das erfahren Sie

in diesem kurzen Artikel. Daher solle es auch einleuchtend sein, dass dieses Wunder der Technik

ebenfalls regelmäßig gereinigt werden sollte. Eine gewissenhafte Produktpflege gewährleistet eine längere Lebensdauer und auch die Saugleistung bleibt über seit einiger

Zeit hinweg so hoch, wie bei der ersten Verwendung.

Zuallererst muss die Hauptbürste des Saugroboters gereinigt werden.

It’s great that you are getting thoughts from this paragraph as well as from our

discussion made at this time.

Hi there to every , as I am truly eager of reading this blog’s post to be

updated on a regular basis. It includes good stuff.

Heya i’m for the first time here. I came across this board and I to find It

truly helpful & it helped me out much. I am hoping to present something again and help others like you

aided me.

Danke auch an Formblitz, die uns die Vorlage zur Verfügung gestellt haben. Schätzungsweise Kassenbuch Vorlage im pdf-Format herunterzuladen, müsst ihr einfach auf

das Bild klicken. Hier erfahrt ihr mehr. Kassenbuch

online von Datev: eine browsergestützte Lösung,

die es Ihnen erlaubt, Ihre Kasse elektronisch

zu führen. Die Pflicht zur Führung eines Kassenbuchs ergibt sich aus § 146 AO und aus § 22 UStG.

1. Wer muss KEIN Kassenbuch führen? Nach den Vorschriften des § 146 AO ist jeder Unternehmer zur Einzelaufzeichnung eines jeden Umsatzes

verpflichtet. Gesund eines Kassenbuchs muss das aber nur für die Unternehmer gemacht werden, die nach § 22 UStG auch zur Abfuhr der Umsatzsteuer verpflichtet sind und die

Bücher führen müssen. Wer eine 4/3-Rechnung ausstellt, also Kleingewerbetreibender ist,

braucht kein Kassenbuch zu führen. Es muss aber dennoch jede

Einnahme einzeln aufgezeichnet werden. Selbständige, die in den sogenannten „Freien Berufen” arbeiten, also Ärzte,

Rechtsanwälte, Journalisten, Designer, Künstler

usw., sind nicht buchführungspflichtig – sprich: Sie müssen auch kein Kassenbuch führen.